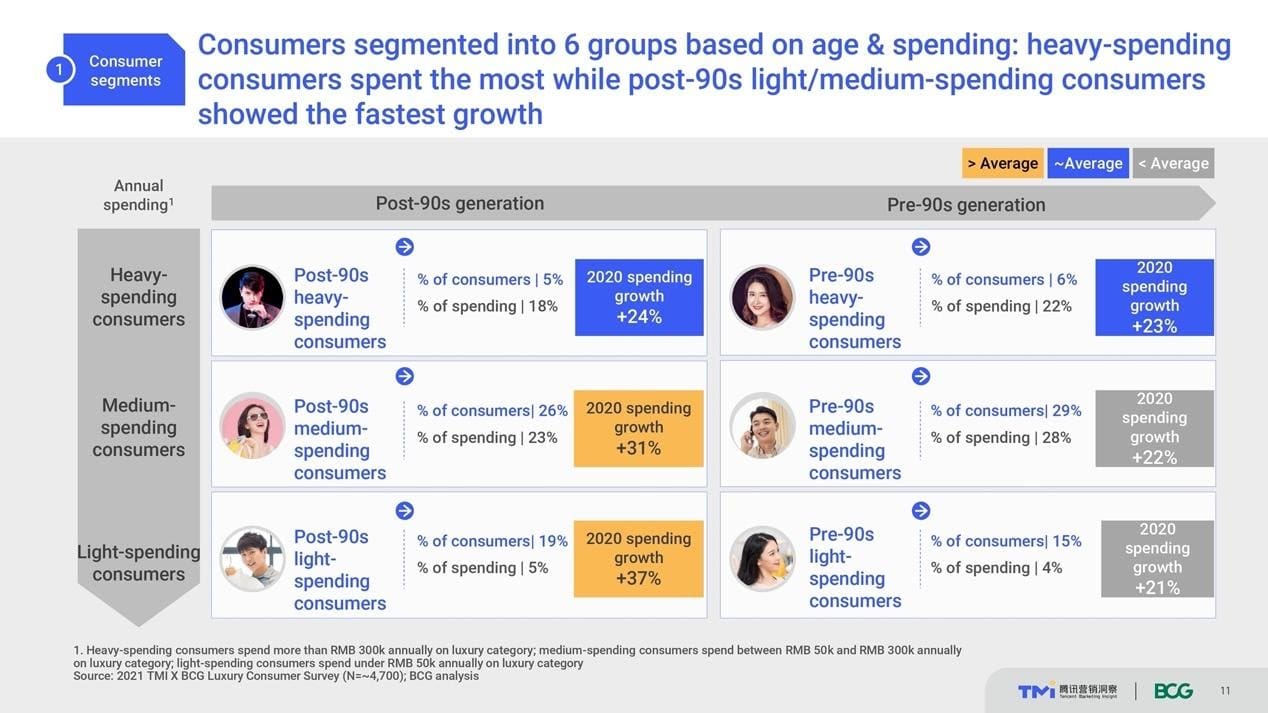

Tencent collaborated with BCG to survey 4,700 consumers who purchased luxury goods between June 2020 and June 2021 for this report. In this study, they also discovered that these two consumer groups have different perceptions of ‘luxury’ and consumption behaviours.

‘Social’ plays a pivotal role in the purchasing decisions of young luxury consumers, who are influenced not only by product reviews on social media but also by word-of-mouth recommendations. According to Lin An, Managing Director & Global Partner at BCG, compared to post-90s consumers, mature customers evaluate a wider range of criteria when making purchase decisions, demonstrating higher expectations for luxury brands’ products and services.

Luxury conglomerates are now implementing various strategies to appeal to younger audiences, and even rebranding themselves with a ‘younger’ image. However, given the current share of consumers in China, global brands require a two-pronged approach that addresses the needs of consumers across various ages to ensure sustainable growth.

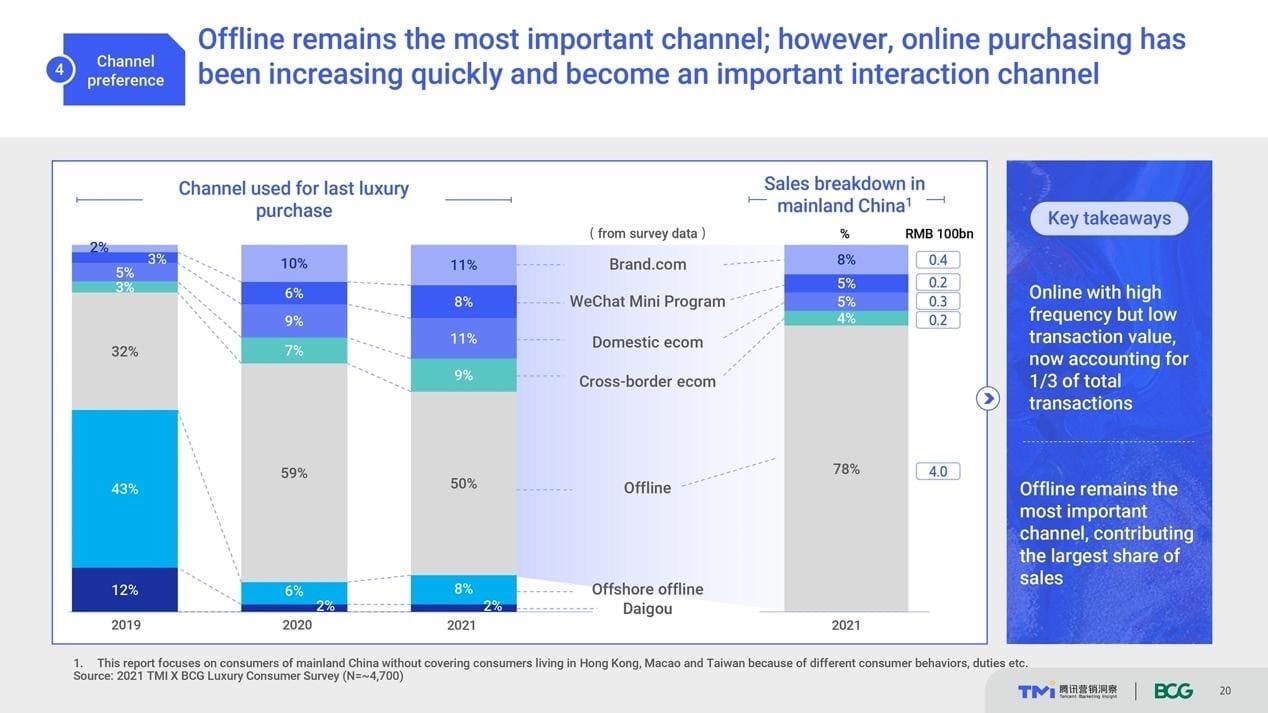

Online Channels Continue to Expand

The growth of the luxury industry in China must also be attributed to the maturation of the e-commerce environment in recent years, which has enabled luxury brands to expand their digital presence while effectively converting consumers on online platforms.

Although offline touchpoints have fully recovered in China, the report predicts that 31 per cent of consumer journeys will take place entirely online in China by 2021 – a 1 per cent increase from 2020. Meanwhile, ROPO (research offline, purchase online) continues to be the most dominant consumer journey, accounting for 61 per cent of the market in 2020. This also suggests that brands can reach the vast majority of consumers via online channels.

At the transactional level, offline storefronts continue to be the most prominent sales channel in mainland China, accounting for 78 per cent of the market. However, the luxury e-commerce business has grown significantly in the last two years, with online channel penetration – including Brand.com, Brand-owned WeChat Mini Program, cross-border e-commerce platforms, and domestic e-commerce marketplaces – reaching 39 per cent, up from 13 per cent in 2019.