Some haute horlogerie names saw search demand grow +25% in 2025. Others surged +21% or climbed +15%. Meanwhile, several mid-range brands fell −8% or worse. The luxury watch market didn’t decline in 2025, it rotated. Demand moved decisively upmarket, rewarding brands with horological credibility and collector cachet while punishing those caught in the accessible middle.

Source: DLG LuxuryIQ MCP

This analysis covers the full calendar year 2025 versus 2024, drawing on LuxuryIQ MCP search demand intelligence across 60+ markets, pre-owned market pricing from 290+ sellers, and social engagement data for 43 watch brands. The data tells a story of rotation, not recession, a market where consumers aren’t searching less, but searching differently.

The Segment Scorecard

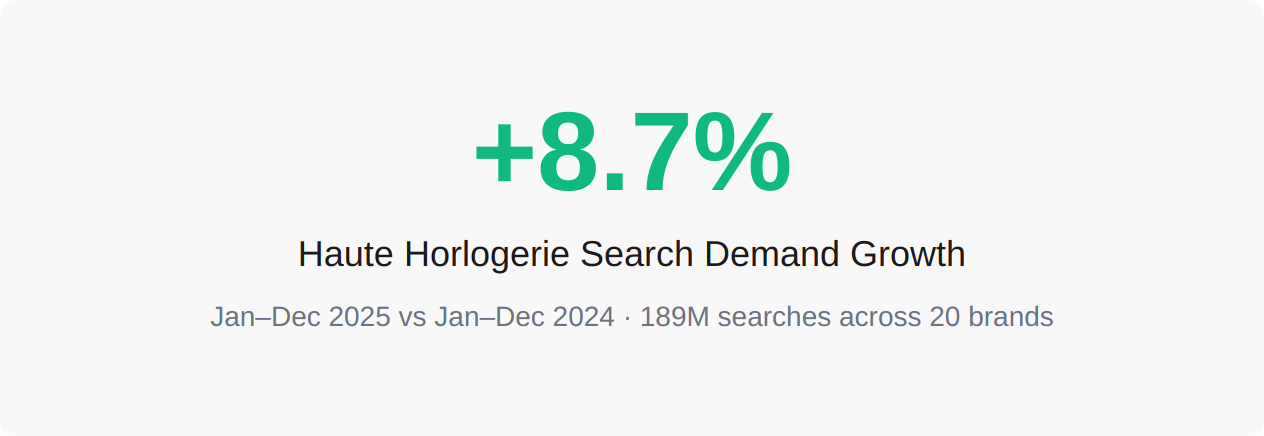

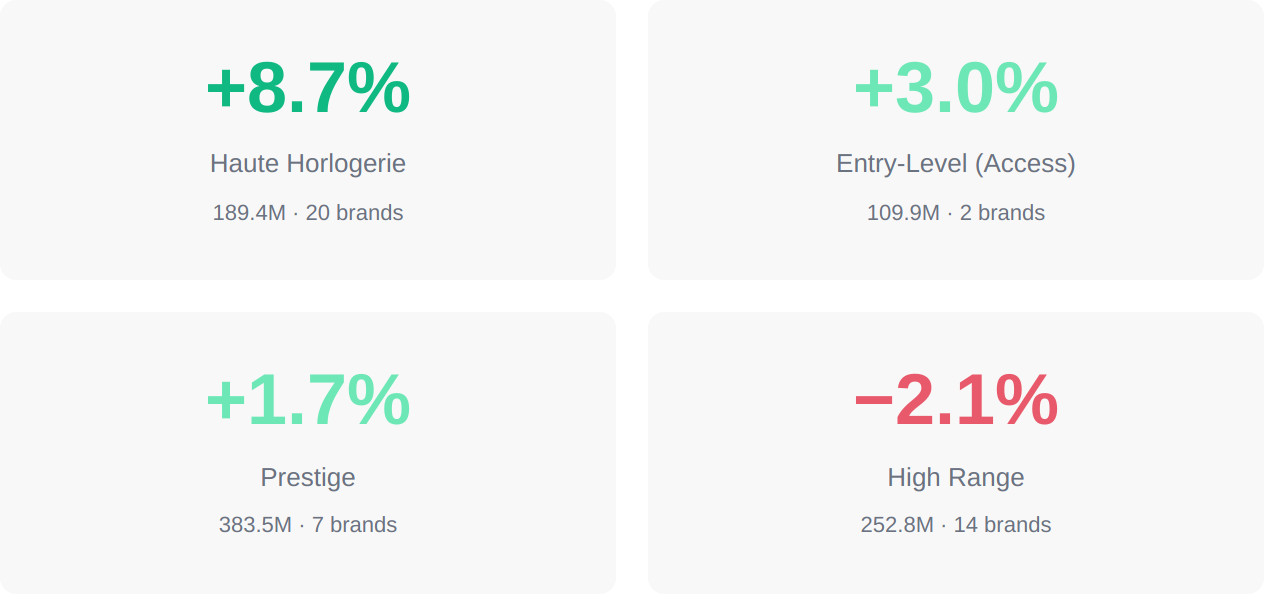

Across the four pure watch segments, total search demand grew +2.1% year-on-year, 935.6M searches in 2025 versus 916.5M in 2024. But the growth was wildly uneven.

Haute Horlogerie led the field at +8.7%, more than four times the blended market rate. Entry-Level (Access) posted +3.0%. Prestige grew a modest +1.7%. And High Range, the only segment in the red, contracted −2.1%. The pattern is clear: the further up the price ladder, the stronger the growth. The segment that asks consumers to pay the most, and delivers the most horological substance, rewarded its brands most handsomely. High Range, where brands compete on heritage and design against the gravitational pull of the Prestige tier above, was the only segment to lose ground.

Source: DLG LuxuryIQ MCP

The Connoisseur Effect

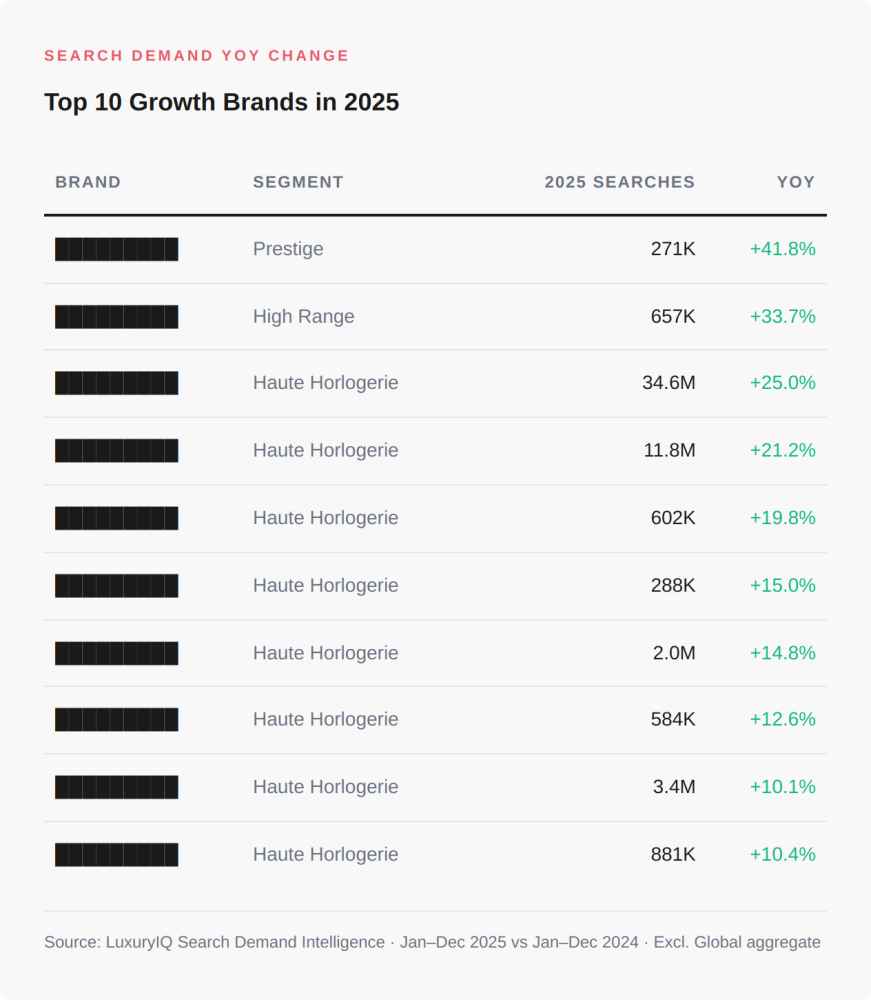

The most dramatic story of 2025 isn’t what happened at the top of the Prestige tier — it’s what happened one tier above. The independent and collector-focused brands posted some of the most aggressive growth numbers in our database.

By percentage growth, the top two names on the leaderboard are actually a small Prestige brand (+41.8% off a 271K base) and a High Range name (+33.7% off 657K searches), proof that exceptional product stories can punch above their segment. But the weight of the growth story sits squarely in haute horlogerie: eight of the top ten growers belong to that tier, and the brand with the most impressive combination of scale and growth posted +25%, propelled by 34.6M searches, remarkable for a brand at that price point. The micro-independents are all posting double-digit gains from smaller bases, signaling a broadening of the collector economy beyond the established names.

Haute Horlogerie: Ultra-high-end manufactures and independents (~$15k–$500k+ retail).

Prestige: Major luxury houses with global scale (~$5k–$50k retail).

The common thread: these are names that collectors discuss in forums, that appear in auction catalogues, and that signal genuine horological literacy. Which brands made the list? LuxuryIQ MCP subscribers see the full brand-level rankings.

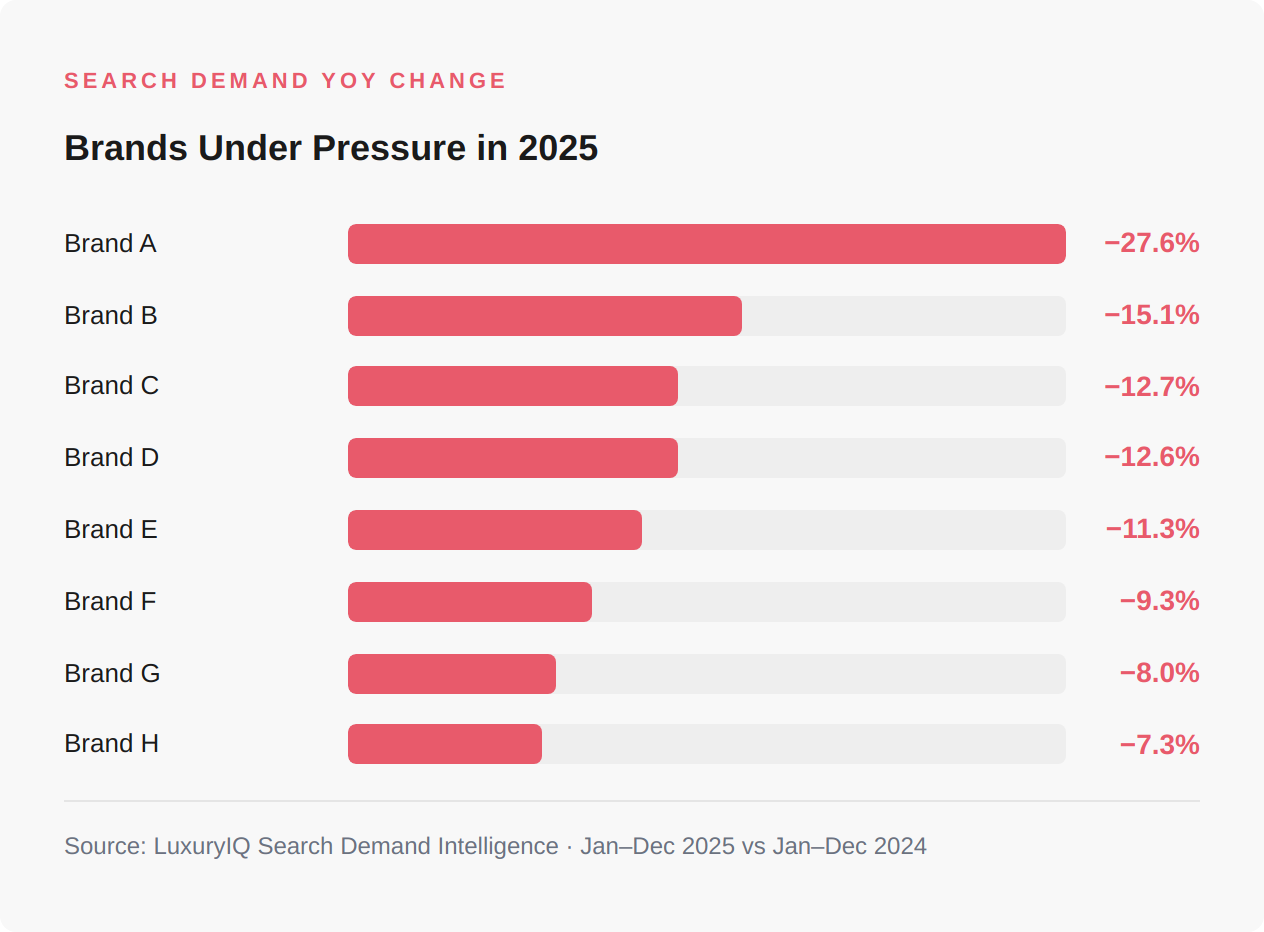

The Squeezed Middle

If the top is thriving, the middle is under pressure. High Range was the only segment to contract, and the brand-level data reveals why.

Brand names redacted. Source: DLG LuxuryIQ MCP

The sharpest declines span every tier. In Access, one brand’s −12.7% decline stands out — a collaboration-driven hype cycle that inflated 2023–2024 search volumes has faded, and the brand is returning to a more organic demand baseline. In High Range, several heritage names fell −7% to −8%, feeling the squeeze from a consumer who, when choosing between a CHF 5,000 watch and saving for something above CHF 10,000, increasingly trades up.

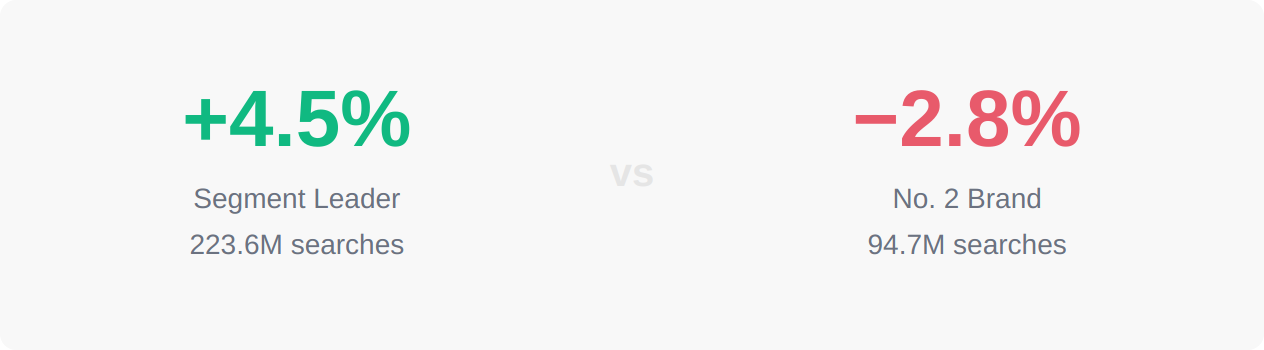

The Prestige Anchors Hold

Prestige, the segment anchored by the market’s largest brand, grew +1.7% overall, but the detail matters. The segment leader grew +4.5% to 223.6M searches, reinforcing its position as the gravitational center of the watch market. But the second-largest Prestige brand slipped −2.8% and another key player dropped −8.3%, suggesting the segment’s growth is driven by its anchor rather than broad-based momentum.

This top-two divergence is significant. Both brands refreshed key collections in 2025, but the segment leader continues to benefit from a scarcity-driven narrative and investment-piece positioning. Its closest competitor, buoyed by major sports and entertainment partnerships, should theoretically be gaining ground, yet the data suggests that when consumers with CHF 5,000–10,000 budgets think “watch,” they increasingly gravitate to the dominant name first.

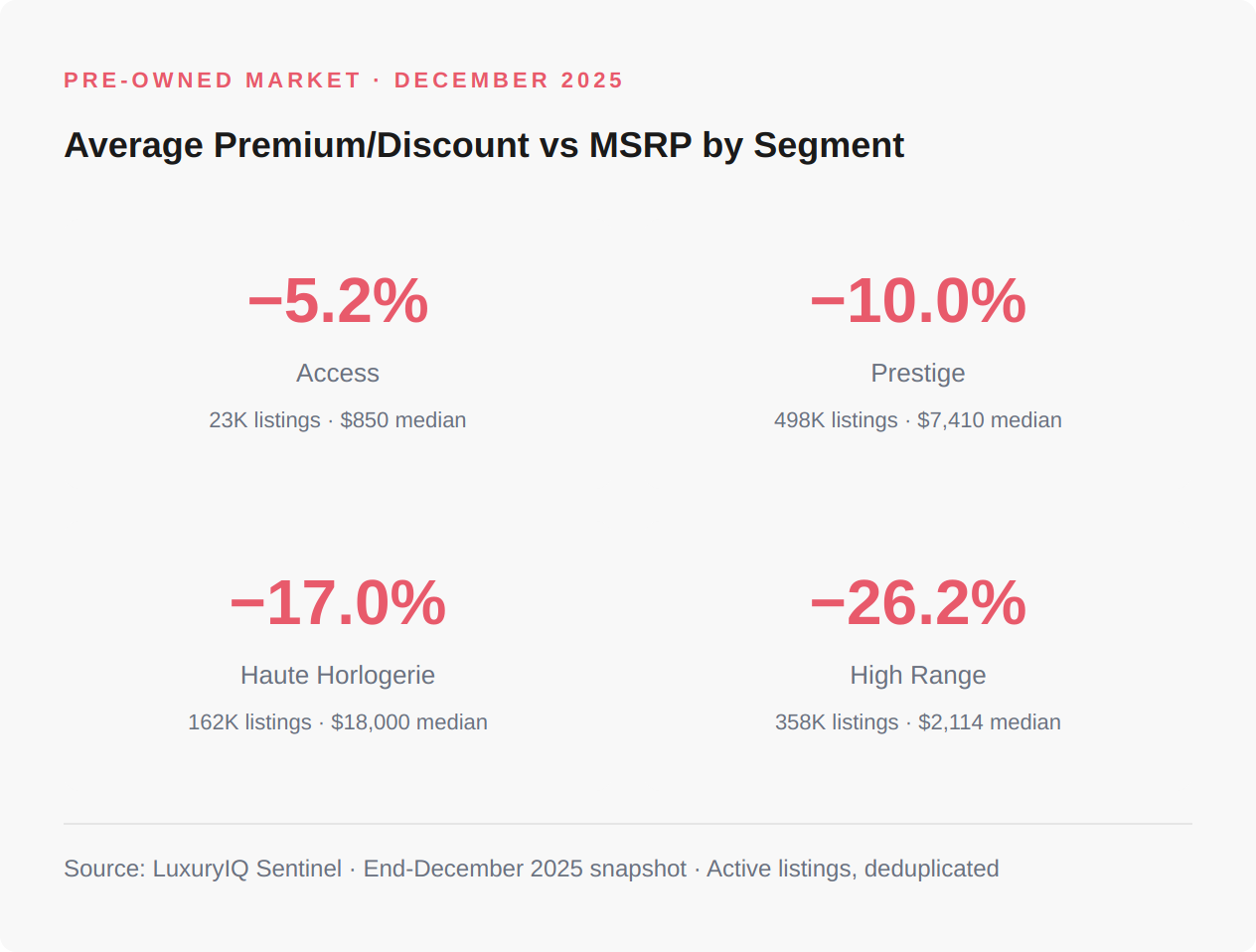

The Secondary Market Paradox

Here’s where the story gets nuanced. Pre-owned prices continue to show discounts to MSRP across every segment, even for Haute Horlogerie brands where search demand is surging.

Source: DLG LuxuryIQ MCP

The paradox: search demand is growing but pre-owned prices remain below MSRP. For Haute Horlogerie, the −17% average discount reflects the post-2022 correction still working through secondary market inventory. What’s encouraging for brands is the direction: these discounts have been gradually narrowing throughout 2025, suggesting the demand surge is beginning to pull prices up. A time-series view of HH discounts, from roughly −22% in Q1 to −17% by December, would confirm the trend, and is something we’re tracking in detail for LuxuryIQ MCP subscribers.

High Range’s −26% discount tells a starker story. With 358K active listings and a median price of just $2,114, the secondary market is flooded with inventory. New buyer demand isn’t absorbing it. For brands in this segment, every pre-owned listing at −26% to MSRP is a competitor sitting on the same retailer’s screen and often the same customer’s wrist.

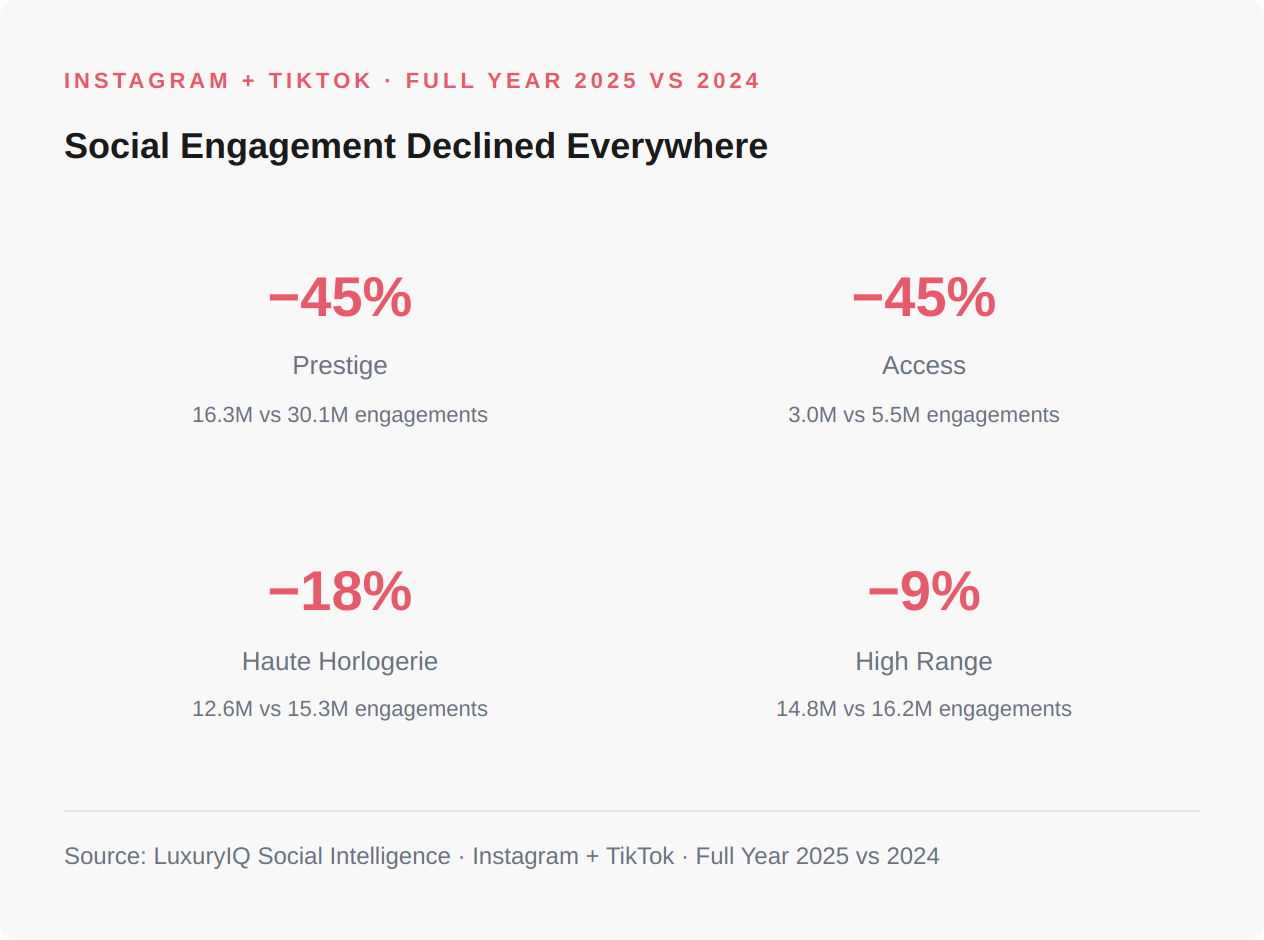

The Social Silence

Perhaps the most counterintuitive finding: while search demand rose, social media engagement fell across every single segment.

Source: DLG LuxuryIQ MCP

These are dramatic numbers: Prestige and Access both fell −45% year-on-year. The scale of the decline, particularly at the top, demands careful interpretation. Some of this is structural: algorithm changes on Instagram and TikTok have compressed organic reach across all categories, not just watches. Posting frequency and content mix also vary by brand and year, which can amplify or dampen engagement independently of audience behavior.

That said, the divergence between rising search intent and falling social engagement is significant and unlikely to be explained by platform mechanics alone. The data suggests a behavioral shift: watch buyers in 2025 are researching more and reacting less, moving from social-media-driven discovery to intent-driven education. A maturing audience that prefers deep-dive research over scroll-through posts may be rendering traditional social KPIs increasingly misleading. Brands still investing heavily in impression-based social strategies may be measuring the wrong thing.

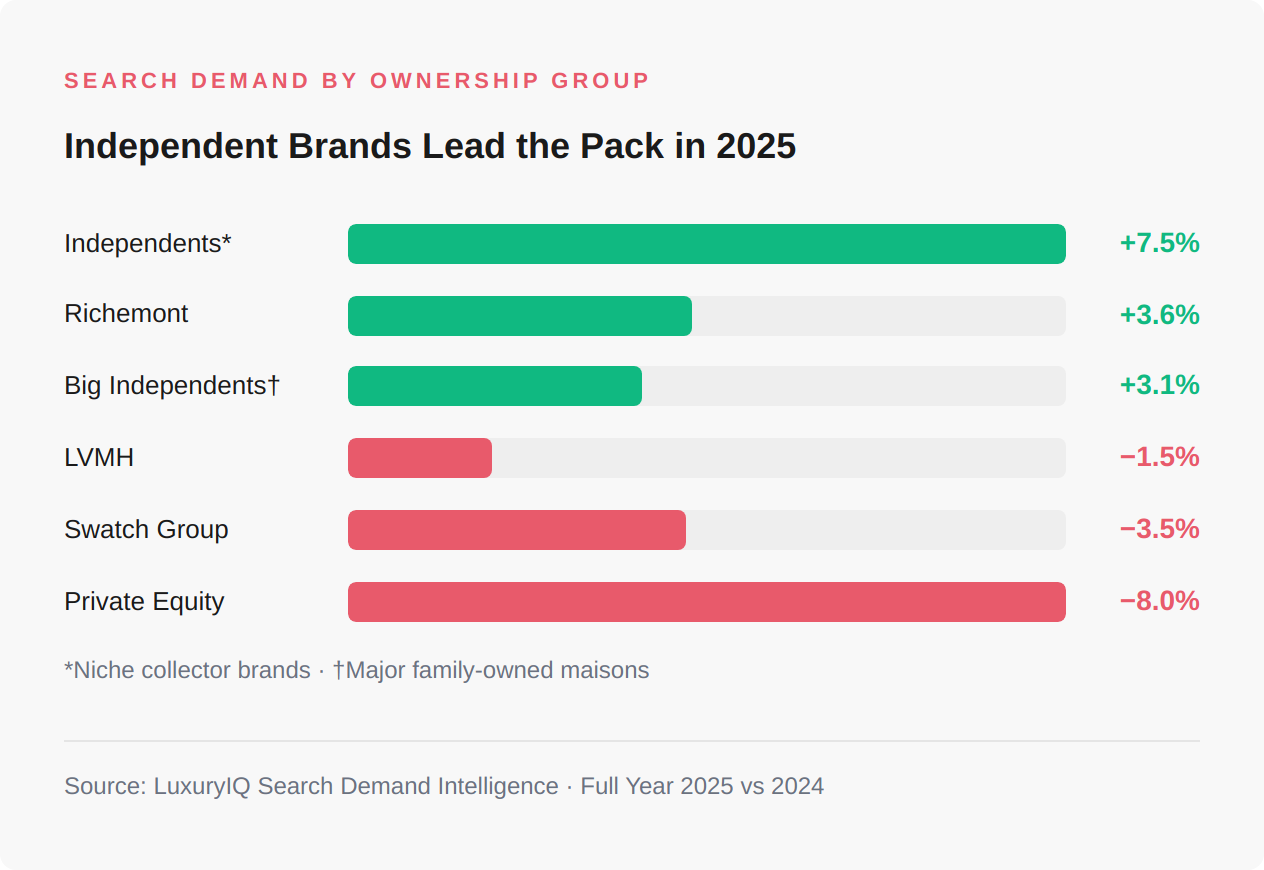

The Conglomerate View

At the group level, the rotation story maps neatly onto ownership structures, though these are blended averages that can mask divergent brand-level stories within each portfolio.

Source: DLG LuxuryIQ MCP

The independent brands, collectively the most horologically pure group, grew at +7.5%, roughly double the rate of the big family-owned maisons (+3.1%). Richemont, buoyed by double-digit growth from its top haute horlogerie names, posted a solid +3.6%. On the other side, LVMH (−1.5%) felt the weight of declining demand across several of its key watch brands, while Swatch Group (−3.5%) was dragged down by softness in its Prestige and Haute Horlogerie stables. Private equity-backed holdings fared worst at −8%, though the small number of brands in this cohort means one or two underperformers can skew the average significantly.

So What?

The 2025 data reveals a luxury watch market that is growing, but growing unequally. The consumer is not retreating; they’re trading up. The brands winning the search wars share a cluster of traits: horological depth, collector credibility, and a narrative that transcends fashion cycles. The brands losing share are those stuck between luxury and accessibility, unable to fully claim either position.

For brands in the haute horlogerie tier, the data validates doubling down on exclusivity and craft. The “connoisseur economy” is expanding, niche independents don’t have massive marketing budgets, yet double-digit demand growth suggests their reputation is doing the work. The strategic implication: these brands should resist the temptation to expand distribution or lower entry prices. The data says the scarcity premium is real and growing.

For brands in the high range, the prescription is harder and more urgent. Secondary market discounts of −26% to MSRP mean the pre-owned market is actively competing against new sales. Search demand contraction compounds the problem. Incremental innovation won’t close this gap. These brands face a strategic fork: invest aggressively in differentiation, proprietary materials, exclusive experiences, community-building that earns collector credibility, or accept a shrinking addressable market. Half-measures risk accelerating the decline.

And for everyone: the social engagement decline, even if partly driven by platform algorithm changes, should prompt uncomfortable questions about where attention is actually moving. Search demand is rising. Social engagement is falling. Whether that’s a permanent behavioral shift or a cyclical correction, the practical implication is the same: brands over-indexed on social impressions as a proxy for desirability may be tracking a metric that no longer reflects how their audience actually discovers and evaluates watches. The smarter move for 2026 isn’t to abandon social, it’s to stress-test whether the current mix of spend and measurement still matches how consumers are actually behaving.

Dominic Weir is Strategy Director at DLG, parent company of The Luxury Society. Based in Geneva, Dominic previously held senior positions at Richemont.

The newly released WeChat Luxury Index examines how high-end and luxury brands achieve marketing or business objectives on WeChat. The report also showcases a ranking of these brands, evaluating whether their offerings and services on WeChat are developed enough to meet the sophisticated demands of today’s consumers.

In an exclusive interview for The Luxury Society Podcast’s inaugural episode, TAG Heuer CEO Antoine Pin reveals how the brand’s historic return to Formula 1 aims to conquer new markets, seduce younger consumers, and win the ultimate battle: The one for our wrists.

At the WEF 2026, the conversation shifted from AI principles to implementation. With DLG’s LuxuryIQ MCP, luxury brands can finally bridge the gap between fragmented data sources and strategic intelligence – transforming how they compete in an AI-driven market.

Luxury’s traditional “white glove” service faces a digital crisis. As technology democratises personalisation, heritage brands must leverage AI and real-time data to anticipate individual needs or risk losing their premium positioning to more digitally savvy competitors.

AI promises to transform luxury, yet most brands remain stuck experimenting. The bottleneck isn’t technical capability – it’s organisational inertia. Fragmented teams, outdated structures, and misaligned metrics prevent companies from translating AI insights into action.

This top-two divergence is significant. Both brands refreshed key collections in 2025, but the segment leader continues to benefit from a scarcity-driven narrative and investment-piece positioning. Its closest competitor, buoyed by major sports and entertainment partnerships, should theoretically be gaining ground, yet the data suggests that when consumers with CHF 5,000–10,000 budgets think “watch,” they increasingly gravitate to the dominant name first.

This top-two divergence is significant. Both brands refreshed key collections in 2025, but the segment leader continues to benefit from a scarcity-driven narrative and investment-piece positioning. Its closest competitor, buoyed by major sports and entertainment partnerships, should theoretically be gaining ground, yet the data suggests that when consumers with CHF 5,000–10,000 budgets think “watch,” they increasingly gravitate to the dominant name first.